Buy-Ins, Buy-Outs and Superfunds

Buy-Ins, Buy-outs and Superfunds (and longevity swaps)

(or ‘How I Learnt about the risk-transfer market and stayed relatively sane’)

Introduction

First of all, some definitions:

- Bulk annuity scheme – this is a way for a defined benefit pension scheme to transfer its risk (‘de-risk’) to an insurance company and can be either a buy-in or a buy-out (see below)

- Buy-in - In exchange for a single premium payment from the trustees, an insurance company will guarantee to pay an income stream (often monthly) to a bank account nominated by the trustees. It has become common for trustees to conduct a series of buy-ins, de-risking the liabilities for different cohorts of members as they retire. This is usually part of a de-risking strategy which ends in the winding up of the scheme following buy-out.

- Buy-out- All legal responsibility for administration, payments and communication to the selected members is taken over by the insurance company. Often, all scheme members are included so that the trustees can wind-up the scheme, but it’s possible to arrange a buy-out for a sub-set of the membership, in which case all groups of members must continue to be fairly treated.

- Superfund - A superfund is a model that allows for the severance of an employer’s liability towards a DB scheme. The transferring employer is replaced by a special purpose vehicle employer to preserve the superfund's Pension Protection Fund (PPF) eligibility and the employer covenant is replaced with a capital buffer consisting of capital from external investors and also an upfront employer payment for entry.

- Longevity Swap - A financial vehicle to protect pension schemes against their pensioners living longer than expected. This is done, in one of the versions of this vehicle, by the pension scheme paying a fixed periodic amount to the scheme provider for an agreed period. If members live longer than assumed, the provider would make a net payment to the scheme. However, if members die more quickly than assumed, the net payment would be paid by the scheme to the provider (more detail – much more detail - in the reference).

All of the above schemes are about transferring risk from the defined benefit pension schemes to other institutions. It will be no surprise that transferring risk in this way is becoming increasingly popular. A recent survey by Hymans Robertson, for example, showed that some 49% of schemes were targeting buy-out in 2020 compared to 15% in 2016.There are currently around £2 trillion of defined benefit liabilities in the UK representing more than 5,000 company schemes. The market is therefore very large for potential providers of these schemes.

Superfunds

At present there are two existing defined benefit superfunds. These are:

- The Pension SuperFund

- Clara-Pensions

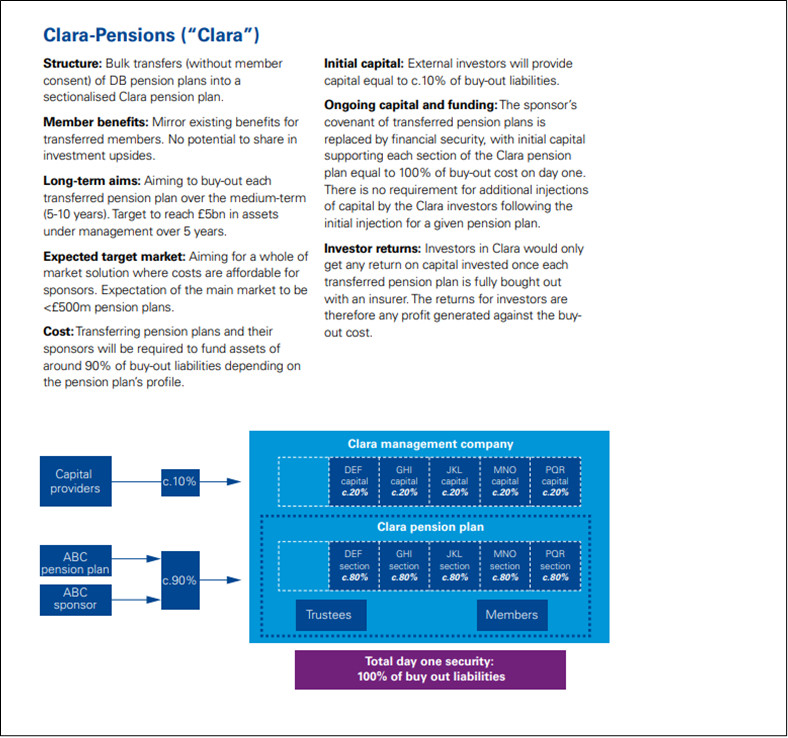

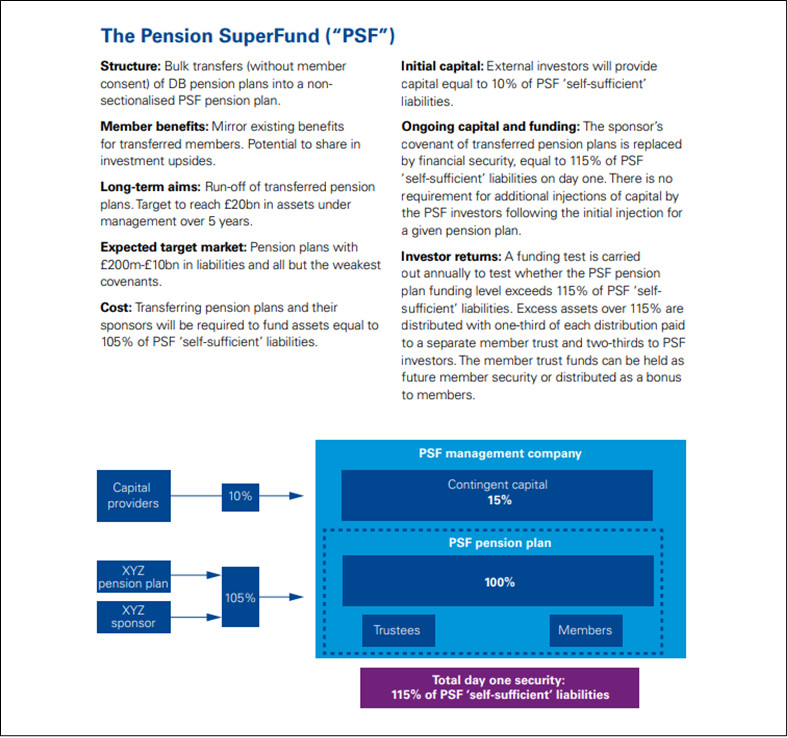

These are explained by these two graphics prepared by KPMG which are at the end of this note.

However, there are many more in development and a recent report by KPMG expects that the market will grow (this reference also has a useful summary of each of the existing superfunds). Currently, however, the pensions industry is waiting for the two existing superfunds to gain approval from The Pensions Regulator (TPR).

It is the view of Pinsent Masons that any transfer of a scheme to a defined benefit (DB) superfund, will need to carried out without members consent and that it is their opinion that this is legally permissible. However, they also say that:

‘Trustees are potentially subject to a higher bar to transfer to a DB superfund than ordinary bulk transfer exercises.

The Department for Work and Pensions (DWP), TPR and PPF have all suggested that trustees will need to be convinced that members' benefits will be more secure in a superfund than under the current scheme, in order to demonstrate that transfer is in members' best interests.

In practice, trustees will need to evidence to TPR as part of the due diligence and clearance process that they are satisfied members' benefits would be more secure in a superfund, which puts significant emphasis on trustees' actuarial and covenant advice.’

(Given TPR’s past record with HPS this may not provide much comfort.)

Once again, much more information is provided in the above reference.

Superfunds work by allowing employers to offload their pension liabilities in return for an up-front payment. The transferring employer is then replaced by a ‘special purpose vehicle’ (SPV) employer in the superfund. This is, effectively, a shell employer put in place to preserve the scheme’s Pension Protection Fund (PPF) eligibility. The former pension scheme’s employer covenant is then replaced with a ‘capital buffer’ made up of capital from external investors and the up-front employer payment.

KPMG have produced a useful table for the pro and cons of superfunds as follows:

|

Pros |

Cons |

|

A sponsor is able to discharge their pension obligations at a lower cost than insurance buy-out, especially in respect of deferred pensioner members |

Current superfund options still require high funding levels and contributions for entry so only available to sufficiently strong pension plans or sponsors |

|

In the right circumstances member security can be increased due to an improved funding position and third-party capital in place of an uncertain employer covenant |

Uncertainty over superfund regulatory regime and the future moral obligations on departing sponsors |

|

Efficiencies and economies of scale provided by dedicated management teams and professional trustee boards with strong governance and risk management |

Complex due diligence process for sponsors and trustees, particularly around sponsor covenant and understanding superfund risks and member benefit security when compared to insurance buy-out |

A con that they appear to have missed out, or at least not stated explicitly, is that they seem to be inherently riskier than insurance-based buy-ins and buy-outs as, unlike the insurance vehicles they are not covered by the Financial Services Compensation Scheme (FSCS) which should cover 100% of the pension if an insurance company fails. However, the TPR has stated that superfunds will only be approved if there is a 99% probability that members' benefits will be paid in full. Nevertheless, a superfund could fail and in that event the scheme would most likely become part of the PPF with a possible cut in benefits for some members.

Finally, the Financial Times article on superfunds has an interesting question within it as follows:

‘Can I stop my pension from being moved to a superfund?’

‘In a word – no. Members are only entitled to be told about such transfers one month before they happen and there is no obligation to consult or get member approval. However, company scheme trustees are required to act in the best interest of members…’

Incidentally, these superfund vehicles are also apparently called ‘Commercial Consolidators’ just to confuse everyone further.

Buy-ins and Buy-outs

Currently, although precise figures are difficult to come by, it seems that some £120.5 billion of the £2 trillion of defined benefit liabilities referenced above have been transferred to buy-in or buy-out schemes. These are operated by eight insurance providers which are: Aviva, Just, Phoenix Life, Rothesay Life, Canada Life, Legal and General, Pension Insurance corporation and Scottish Widows.

Some large companies have transferred their schemes to buy-ins and buy-outs as follows:

- Rolls Royce (£4.6 billion buy-out)

- Vickers (£1.1 billion buy-out)

- British Airways (£4.4 billion buy-in)

- ICI (completed its 17th buy-in in 2020 amounting to £9 billion of liabilities)

- TRW Automotive (£2.5 billion partial buy-out)

- Siemens (£1.3 billion buy-in)

- ASDA (£3.8 billion buy-in)

A list of the biggest buy-ins and buy-outs since 2007 can be found here. Many of these buy-outs are what is known as PPF+ transactions. This is when a scheme enters the PPF assessment period but instead of entering the PPF is transferred to an insurance company. An example of such a transaction with the Mowlem pension scheme can be found on the Legal and general website. Some of the pros and cons of insurance-based buy-outs are as follows (from here):

|

Pros |

Cons |

|

Strong level of benefit security for members |

High entry cost and less competitive for market for buyouts of less than £50M |

|

Meets primary trustee objective of permanent solution to meet benefits in full |

Cost can be high due to reserving requirements (especially in respect of members who have not yet retired) |

|

Well-tested regime – decades of experience without any defaults or reductions to annuity payments |

Some (very limited) benefit features not suitable for insurance, e.g., long-term link to salary |

|

Ongoing monitoring by the Financial Conduct Authority |

Permanent decisions need to be made on the treatment of any discretionary benefits |

|

Detailed contractual terms providing protection for trustees |

Need to consider the accounting implications for sponsors |

Some of the pros and cons of insurance-based buy-ins are as follows (from here):

|

Pros |

Cons |

|

Strong level of security (as per insurance buyout) although not allocated to the individual |

Annuity purchase requires sufficient assets up front to secure the scheme liabilities and less competitive for market for buyouts of less than £50M |

|

Well-tested regime with existing governance procedures around treating members fairly |

Permanent allocation of assets to annuity purchase, and so no potential for any future gain on assets or strategic investment changes in respect of assets used to fund the buy-in |

|

Members still ultimately able to rely on the sponsor's covenant as well as the insurer |

Cost can be high due to reserving requirements (especially in respect of members who have not yet retired) |

|

Ability to incrementally secure benefits when affordable, rather than waiting until the scheme as a whole can be secured |

Residual risks are uninsured |

|

Fewer accounting implications for sponsors |

A buy-in provides ‘double covenant’ protection of the associated benefits (from the insurer and from the continuing sponsor) which can make it difficult in some circumstances to convert to a buyout |

Longevity Swaps

These sound a bit wimpy but the value of some of them can be very high. The BT pension scheme carried out a £14 billion longevity swap in 2014 while the Lloyds banking group’s swap in 2020 amounted to some £10 billion. A list of the largest longevity swaps since 2009 can be found here.

There are essentially two flavours of longevity swaps known as ‘Named Lives Swaps’ and ‘Population Index Swaps’. Anyone desperate to know more about longevity swaps should read this Barnett-Waddingham web page.

Pension Superfund (from KPMG)

Clara Pensions (from KPMG)